Reading time:

What is an SEC Filing?

Learn what SEC filings are, their purpose, and how investors, companies, and analysts use 10-Ks, 10-Qs, 8-Ks, and more to ensure transparency and regulatory compliance.

Article written by

Jared

Definition and Purpose of SEC Filings

An SEC filing is a formal document that companies, insiders, and other regulated entities are required to submit to the U.S. Securities and Exchange Commission (SEC). These filings are designed to provide investors, regulators, and the public with standardized, comparable, and timely information about a company's financial condition, operations, governance, and material events. The overall purpose is to promote transparency, reduce information asymmetry between insiders and the investing public, and support the integrity of U.S. capital markets.

SEC filings cover a broad spectrum of disclosures: routine periodic financial reports, current event notices, ownership reports by large shareholders, proxy statements for shareholder votes, registration statements for new securities offerings, and whistleblower or enforcement-related communications. Each filing type has a statutory or regulatory basis, standardized formats, and often specific timing requirements to ensure the information reaches the market promptly.

Because filings are legal documents submitted under federal securities laws, they carry legal significance. Information in filings may be relied upon by investors and regulators; inaccuracies, omissions, or late filings can expose a company or individuals to regulatory enforcement actions, shareholder litigation, or reputational harm. For that reason, public companies typically have cross-functional processes—finance, legal, investor relations, and disclosure committees—to prepare, review, and certify filings.

Key Types of SEC Filings

Several filing forms appear with high frequency and are essential to understanding corporate disclosure regimes. Among the most significant are:

Form 10-K: The annual comprehensive report (discussed in detail below).

Form 10-Q: The quarterly report providing interim financials.

Form 8-K: The current event report for material developments.

Schedules 13D and 13G: Beneficial ownership reports filed by investors acquiring more than 5% of a company's equity securities.

Proxy statements (DEF 14A): Documents sent to shareholders describing matters to be voted on at annual or special meetings.

Each of these filings serves a different audience and purpose. For example, Form 10-K delves into audited financial statements and management's long-form discussion, while Form 8-K is used to swiftly notify the market about discrete, material events such as mergers or executive changes. Schedules 13D/13G are targeted at revealing ownership concentrations and the intentions of significant shareholders.

Knowing which form to consult depends on the investor's objective: long-term fundamental analysis, short-term event-driven trading, corporate governance research, or regulatory compliance checks all point to different filing types as primary sources.

Form 10-K: The Annual Report in Detail

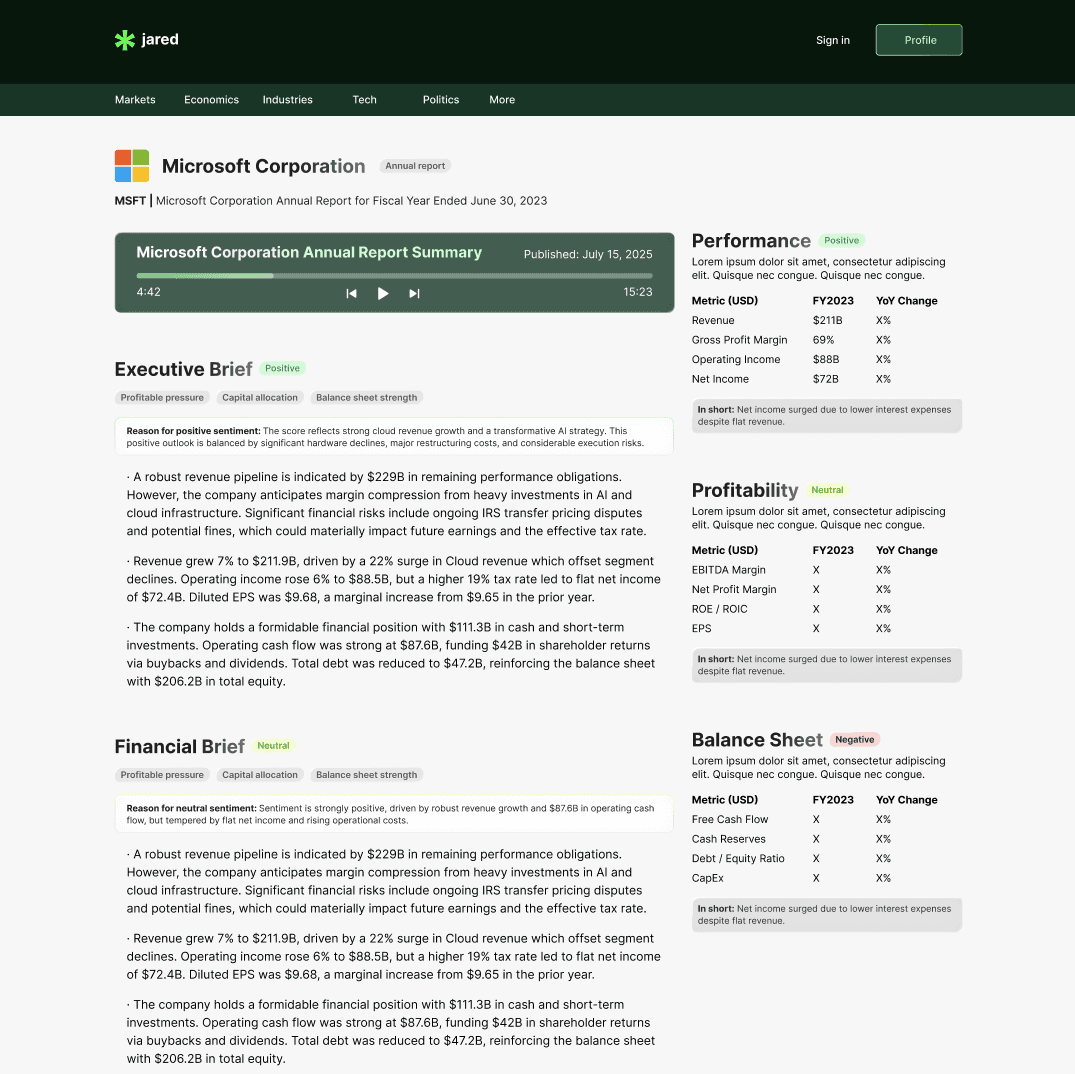

Form 10-K is the most comprehensive annual filing that a public company must file with the SEC. It contains audited financial statements, notes to the financials, management's Discussion and Analysis (MD&A), and extensive disclosures about business operations, risk factors, legal proceedings, executive compensation, and corporate governance. The 10-K functions both as a compliance document and a primary research source for analysts and institutional investors.

The MD&A section in a 10-K is particularly valuable because it offers management's narrative about the company's financial performance, trends, liquidity, capital resources, and known uncertainties. Risk factors enumerate threats that could materially affect the company's business, and these must be updated annually to reflect new or evolving risks. Because the financial statements are audited, the 10-K also includes audit opinions and any material weaknesses in internal controls if identified.

10-Ks are certified by senior executives—typically the CEO and CFO—under the Sarbanes-Oxley Act, creating statutory attestations about the accuracy of the financial statements and the effectiveness of internal controls. This legal certification step elevates the responsibility for accuracy and creates potential personal liability for false certifications.

Form 10-Q and Interim Reporting

Form 10-Q is the quarterly report required for each of the first three fiscal quarters for most public companies. Unlike the 10-K, 10-Qs contain unaudited financial statements and focus on interim performance and developments. Key components include condensed financial statements, updates to MD&A from the 10-K, market risk disclosures (if material changes occur), and legal proceedings updates.

Quarterly filings are typically less exhaustive than annual reports but are critical for monitoring trends, seasonality, and changes in liquidity or leverage between annual cycles. Analysts often use 10-Qs to update earnings estimates, reassess guidance, and track management commentary for signaling future corporate actions. The timeliness of 10-Q submissions contributes to market efficiency by ensuring that material operating information is disclosed throughout the year rather than only once annually.

Because 10-Qs are unaudited, they may carry greater short-term revision risk. However, their requirement keeps a cadence of disclosure that supports investor monitoring and enforcement oversight.

Form 8-K: Reporting Material Events

Form 8-K is the mechanism companies use to inform the market of material events that occur between periodic filings. These events include, but are not limited to, mergers and acquisitions, entry into or termination of material contracts, changes in executive officers or directors, restatements of financials, bankruptcy proceedings, and certain financial results or credit agreements.

The timeliness standards for 8-K filings are strict; typically, a material event must be disclosed on Form 8-K within four business days of the triggering event. The short deadline is intended to limit windows during which insiders may have material, undisclosed information. Because 8-Ks often precede stock-price-moving announcements, they are closely watched by traders, analysts, and governance researchers.

8-K reports are structured around item numbers that correspond to different categories of material events. A single 8-K can include multiple items. Companies often use exhibits in 8-K filings to attach underlying agreements, press releases, or other supporting documents to provide full context for the disclosure.

Beneficial Ownership Reporting: Schedules 13D and 13G

Schedules 13D and 13G are filed by individuals or entities that acquire beneficial ownership of more than 5% of a company's class of equity securities registered under the Exchange Act. These schedules inform the market about the identity of significant owners and their intentions—whether passive investment or active engagement seeking control or corporate change.

The SEC has recently tightened the timing and amendment obligations for these reports. Under the 2025 amendments, filers must amend Schedules 13D and 13G within 45 days after the end of the calendar quarter in which any material change occurred, accelerating updates to ownership information and intentions. The change aims to improve transparency around concentrated ownership and activist activity that can materially affect corporate strategy and market expectations.

13D filers typically disclose more detailed information, including plans or proposals concerning the issuer, while 13G is a shorter form filed by passive investors who do not intend to influence control. Both require updates for purchases or dispositions that change beneficial ownership above relevant thresholds, but the new amendment tightens the calendar for amendments to enhance market awareness.

EDGAR and Filing Infrastructure

The SEC's Electronic Data Gathering, Analysis, and Retrieval system (EDGAR) is the central repository and distribution platform for SEC filings. EDGAR provides public access to filings, supports research and compliance workflows, and processes submissions from reporting entities. As of May 25, 2025, EDGAR has processed over 17 million filings, reflecting the system's scale and centrality to U.S. capital markets.

The SEC is modernizing EDGAR with a multi-year upgrade program called "EDGAR Next," which includes new account management, multifactor authentication for filers, and enhanced data standards. The modernization is designed to strengthen cybersecurity, improve the user experience, and better structure filings to support machine-readable data. The compliance deadline for key EDGAR Next requirements is September 15, 2025.

EDGAR's evolution also affects how analysts, vendors, and regulators consume disclosure data. More structured and authenticated filings should improve the reliability of third-party financial data feeds and the automation of compliance checks across financial institutions and advisory firms.

New and Emerging Disclosure Requirements (2025)

The SEC continues to refine disclosure rules to address evolving market practices and governance expectations. A notable 2025 development requires companies to disclose whether they have adopted insider trading policies and procedures governing the purchase, sale, and other dispositions of securities by directors, officers, and employees. If a company has not adopted such a policy, it must explain why in the Form 10-K. This disclosure aims to strengthen transparency around internal controls designed to prevent unlawful trading and to align investor expectations across issuers. Industry guidance regarding these disclosures is available from law firms and governance advisors.

Other recent enhancements focus on accelerating the cadence of ownership disclosures, improving the quality of climate and ESG-related disclosures in some contexts, and increasing the use of structured data to make filings more machine-readable. These changes reflect the SEC’s broader objectives of modernizing filing systems and elevating the completeness and timeliness of information available to market participants.

For preparers, these developments mean updating disclosure controls, legal policies, and IT infrastructure. For users—investors, researchers, and regulators—these changes promise better quality and timeliness of corporate information, albeit during a transition period where legacy and new systems coexist.

Who Files SEC Documents and When

Different parties are required to file with the SEC depending on the nature of the transaction or relationship with the reporting company. Public companies, registered investment advisers, broker-dealers, mutual funds, and individuals or entities meeting ownership thresholds are common filers. Insiders such as officers, directors, and large shareholders must also file periodic reports (e.g., Forms 3, 4, and 5) disclosing their transactions in company securities.

Timing rules vary by form. Annual reports (Form 10-K) follow strict due dates based on the filer’s issuer category (large accelerated filer, accelerated filer, etc.). Quarterly reports (Form 10-Q) are due within a specified number of days after quarter-end, and current reports (Form 8-K) generally must be filed within four business days of material events. Schedules 13D and 13G have immediate filing and amendment rules tied to acquisition dates and subsequent changes, with recent amendments adjusting the cadence for amendments.

Filing deadlines and categories are significant because they determine when information becomes public and when insiders must cease trading on material nonpublic information. Compliance teams within issuers track these dates closely and often use third-party compliance platforms integrated with EDGAR to automate submission workflows and calendar reminders.

How Investors and Analysts Use SEC Filings

Investors and analysts rely on SEC filings as primary-source material for financial analysis, valuation, corporate-governance assessments, and event monitoring. A 10-K provides deep background for building long-term financial models, 10-Qs update assumptions and track recent operational trends, and 8-Ks can signal transformative events such as acquisitions or leadership changes that necessitate immediate reassessment of valuations and risks.

Ownership filings like 13D/G inform activist-investor activity and potential proxy contests. Proxy statements (DEF 14A) reveal executive compensation structures, shareholder proposals, and board composition—critical inputs for governance-focused investors. Analysts often triangulate disclosures across forms to confirm facts, identify inconsistencies, and detect risks not apparent in headline metrics.

Because filings are searchable through EDGAR and increasingly available in structured formats, quantitative investors and data vendors build automated pipelines to ingest filing data for scoring models, risk screening, and news detection systems. High-quality filings are thus foundational for both fundamental and quantitative investment processes.

Legal and Compliance Considerations

SEC filings are governed by federal securities laws and agency rules; inaccuracies, misleading statements, or failures to disclose material information can lead to enforcement actions, fines, or shareholder lawsuits. The Sarbanes-Oxley Act added criminal and civil penalties for certifying false financial reports and required enhanced internal control reporting for public companies.

Compliance teams must ensure that disclosures are complete, accurate, and timely. This involves cross-functional review cycles, document retention practices, and controls over who can access material nonpublic information. The EDGAR Next modernization—requiring individual accounts and multifactor authentication—adds an additional security layer to control who submits filings and when, reducing the risk of unauthorized access or filing errors.

Lawyers, auditors, and investor relations professionals play complementary roles in drafting, reviewing, and communicating filings. External counsel often provides interpretations of disclosure obligations, while auditors give assurance over historical financial statements. Effective coordination among these stakeholders is essential to manage legal risk and maintain investor trust.

How to Access and Search SEC Filings

The primary portal for accessing SEC filings is the EDGAR database, which allows public searching and retrieval of filings by company name, CIK (Central Index Key), form type, and filing date. Many financial data vendors and research platforms build on EDGAR to provide enhanced search, tagging, and analytics functionalities for users who require large-scale or historical searches.

For practical use, investors often set up alerts for specific companies, form types, or keywords (e.g., "material weakness," "change in control," "merger agreement"). Because filings are time-stamped, users can monitor filings in near real-time and react to material events quickly. Some academic and practitioner research also relies on bulk EDGAR downloads for empirical studies of disclosure practices and market responses.

When using EDGAR or vendor interfaces, it’s important to validate that a filing is complete and that attached exhibits are present. Exhibits frequently contain critical agreements and disclosures (e.g., employment agreements, loan contracts, merger agreements) that add legal and economic context not always fully summarized in the body of the filing.

Practical Tips for Reading and Interpreting Filings

Reading SEC filings effectively requires focus on both quantitative and narrative sections. Key quantitative areas include balance sheets, income statements, cash flow statements, and footnote disclosures. Narrative sections—MD&A, risk factors, and legal proceedings—reveal management’s perspective and potential red flags that may not be quantifiable immediately.

Some practical reading tips: start with the most recent 8-K for event-driven issues, scan the 10-Q for recent quarter performance, and consult the 10-K for historical context and governance details. Review management certifications and auditor opinions to assess reliability, and always check exhibits for underlying contractual terms that could materially affect valuation or risk.

Because filings can be dense, many readers rely on executive summaries, highlighted disclosures, or third-party analyses for quick orientation. However, for critical decisions, reading the primary source filing and relevant exhibits is essential to avoid reliance on incomplete or interpreted summaries.

Summary: Why SEC Filings Matter

SEC filings are foundational documents for market transparency, investor protection, and regulatory oversight. They create a public record of a company's financial health, material events, ownership structure, and governance practices. By standardizing and timing disclosures, filings help level the informational playing field for market participants and support efficient capital allocation.

Recent regulatory updates in 2025—such as accelerated amendment windows for beneficial ownership reports, EDGAR modernization with enhanced security protocols, and new disclosure requirements for insider trading policies—underscore the evolving nature of disclosure obligations and the ongoing emphasis on timely, trustworthy information.

For investors, analysts, and corporate practitioners, understanding SEC filings and the systems that host them is essential to making informed decisions, maintaining compliance, and engaging constructively in capital markets.

This content is for general information only and isn’t financial advice. Always do your own research and speak with a qualified advisor before making investment decisions. We can’t guarantee accuracy or outcomes, and you’re responsible for your own choices.

Article written by

Jared

Financial reports summarized by AI

No more 90-page PDF.